Visualizing how resting limit orders construct the bid-ask matrix within an order book. Source: FXSSI

When you open a trade on your terminal, your order fills almost instantly at the exact price you requested. It is easy to take this seamless execution for granted, imagining the foreign exchange market as a giant, automated machine that matches buyers and sellers effortlessly. In reality, behind every stable quote and lightning-fast execution stands a dedicated group of institutional participants working around the clock to grease the wheels of global commerce. Without these specialized institutions, retail portfolios would constantly face grinding price caps, massive processing delays, and unviable transaction costs.

What exactly is a market maker and what do they do?

A market maker is a heavy institutional participant—typically a tier-one global investment bank or a massive financial clearinghouse—that actively quotes both a buy and a sell price for a specific asset class. Instead of waiting passively for an independent buyer and seller to find each other across decentralized networks, these institutions step forward to act as the permanent counterparty to any trade.

They stand ready to buy from you when you want to sell, and they sell to you when you want to buy. Think of them like a traditional wholesale merchant who keeps a warehouse permanently stocked with inventory. You don’t have to wait for another retail shopper to sell you a single box of goods; you simply buy it straight from the distributor’s shelf on demand, ensuring business keeps moving without programmatic friction.

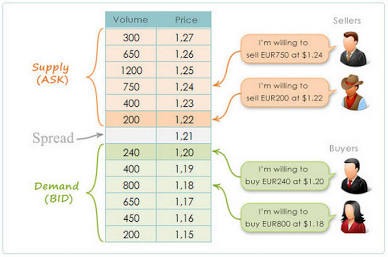

How do market makers create “liquidity” on my chart?

In the context of active currency trading, liquidity represents your ability to convert a market position into cash instantly without causing a massive, disruptive distortion in the asset’s underlying price. Market makers create this fluid environment by continuously pouring millions of dollars of resting limit orders into the centralized matching ledger.

This continuous layer of orders pads the order book, creating a dense safety cushion across changing price coordinates. When you run your daily setups inside an account ecosystem supported by top-tier low spread forex brokers, you are tapping directly into this deep reservoir of institutional supply. The massive volume prevents individual retail tickets from shifting the broader market curve, letting you enter and exit positions without fighting heavy structural roadblocks.

What is the connection between market makers and the bid-ask spread?

The entire pricing matrix on your workspace is a direct reflection of market maker activity. Every financial instrument features a split pricing layout: the bid, which is the highest rate a buyer offers to purchase an asset, and the ask, which is the lowest price a seller demands to let it go.

The gap between these two boundaries forms the spread, which serves as your immediate cost of stepping onto the playing field. This gap functions exactly like an administrative processing charge or entry toll paid to clear your path into a position. When multiple major institutional desks are active, they compete aggressively against one another to capture order flow, which naturally forces their quotes closer together. This institutional battle strips away artificial premiums and compresses your transactional friction down to razor-thin decimal layers.

How do these institutions manage their risk when the market moves against them?

Acting as the mandatory counterparty means market makers routinely absorb toxic, losing positions onto their corporate balance sheets. They don’t simply hold these exposures blindly and gamble on direction; they run highly automated internal risk mitigation programs.

If a wave of aggressive retail buying floods their network, the market maker accumulates a massive short inventory. To balance their books, they instantly push their surplus risk out to broader interbank clearing lines or hedge the exposure utilizing correlated derivative contracts. They survive entirely on the microscopic statistical edge generated by the bid-ask gap across millions of round-turn tickets a day. This mechanical volume-driven model is why gaining a complete grasp of what is a spread in trading gives you an honest, data-driven look into how global institutions monetize order flow.

Why do spreads still expand aggressively during major economic announcements?

The structural order book behaves exactly like a live thermometer for global risk, which means it responds dynamically to real-time macroeconomic shockwaves. When a high-impact news drop—like a central bank interest rate shift or an unexpected employment report—reaches international wires, institutional pricing analysts face massive valuation uncertainty.

To protect their corporate capital from sudden, unhedged gaps, automated market-making algorithms instantly pull their resting limit orders out of the matching ledger. This rapid programmatic retreat leaves a hollow shell behind inside the digital exchange framework. When an incoming retail market order hits this sparse ledger, the platform has to travel across multiple empty pricing layers to secure a match, causing the active spread to stretch defensively like a rubber band until the macroeconomic panic subsides.

How does my platform’s routing infrastructure affect my access to this liquidity?

The processing efficiency of your trading setup relies heavily on the specific plumbing your intermediary uses to route your data packets. Primitive, retail-grade platforms often suffer from slow server links, causing your orders to arrive late at primary institutional matching hubs.

Sourcing an enterprise-grade terminal, such as the best forex broker for mt5, ensures your frontend routes straight through advanced cloud servers co-located right next to prime data center grids. Advanced execution infrastructure pools live feeds from dozens of competing market makers simultaneously. This multi-bank aggregation ensures that even if a few massive clearers pull back their books during a volatility spike, other connected desks remain open to fill your parameters cleanly without severe execution delays or catastrophic terminal freeze-ups.

Practical Action Plan

Stop viewing your charting workspace as a cost-free playground, and start treating it as a highly structured electronic auction house governed by institutional supply and demand. Review your performance log history this weekend, map out the exact times your trades suffer from unexpected slippage or wider entries, and cross-reference those anomalies against global session clocks. By restricting your high-volume execution exclusively to the peak overlap windows of the London and New York sessions, you can ensure your strategy executes when market maker competition is at its absolute densest, locking in the lowest possible transaction costs for your business.